Food Manufacturers

The R&D Tax Credit Explained

The Research & Development (R&D) Tax Credit is a federal (and sometimes state) incentive that rewards companies for developing new or improved products, processes, formulas, or techniques. Food manufacturers often conduct qualifying activities during product development, process improvement, scaling production, or meeting regulatory standards.

You don’t need a lab coat or patent to qualify—many day-to-day operations in food innovation and optimization are eligible.

QUALIFYING ACTIVITIES

Many core functions in a food manufacturing operation qualify for the credit, especially those involving:

- Developing new food or beverage products

- Improving taste, texture, shelf life, or nutritional content

- Experimenting with new ingredients or substitutions (e.g., allergen-free, plant-based, organic)

- Creating formulations to comply with dietary or regulatory standards

- Scaling recipes from test kitchen to commercial production

- Reducing waste or improving yields during production

- Designing or refining automated manufacturing processes

- Testing new packaging solutions for freshness or stability

- Troubleshooting flavor, consistency, or microbial issues

If your team is solving technical problems through trial and error, it likely qualifies.

WHAT cAN BE CLAIMED

Qualified Research Expenses (QREs) include:

- Employee wages: Salaries for R&D chefs, food scientists, QA, process engineers, and operations staff involved in R&D.

- Supplies and ingredients: Used in test batches, pilots, failed runs, or non-commercial prototypes.

- Contract research: Outsourced testing, third-party labs, or consultants (up to 65% of cost).

- Software: Tools used for nutritional analysis, shelf-life simulation, or production modeling.

Pilot production runs: As long as they are pre-commercial and for experimental purposes.

WHAT DOESN'T QUALIFY

The credit doesn’t cover routine activities or anything not involving technical uncertainty or experimentation. Examples include:

- Routine recipe adjustments for taste preference

- Marketing research or consumer focus groups

- Cosmetic changes (e.g., color, packaging design without technical improvement)

- Compliance-only activities (e.g., labeling or non-technical regulatory filing)

- Post-commercial production runs

- Duplicating existing formulas or off-the-shelf products

HOW THE CREDIt WORKS

The R&D tax credit provides a dollar-for-dollar reduction in federal income tax liability.

Two key uses:

- Offset federal income tax – Common for profitable manufacturers.

- Offset payroll tax – For startups (under 5 years old and <$5 million in gross receipts), up to $500,000 per year.

Unused credits can be carried forward up to 20 years.

Average R&D Tax Credit for Food Manufacturers

While it varies based on company size, scope of innovation, and documentation:

- Small to mid-sized food companies: ~$25,000–$100,000 annually

Large manufacturers: $250,000 to $1M+ annually

For Small to Mid-Sized Food Companies

These companies often qualify for credits through:

- In-house product development and testing

- Small batch or pilot production

- Shelf-life or packaging trials

- Label reformulation (e.g., low sodium, gluten-free)

Even without a formal R&D department, many companies qualify based on culinary team work or QA/production staff time.

For Larger Food Manufacturers or Multi-Plant Operations

Larger operations benefit from:

- Dedicated food science or R&D teams

- Centralized pilot labs or test kitchens

- Ingredient and supply chain innovation

- Sustainable process redesign

- Automation and yield optimization

With proper documentation and tax planning, larger firms may claim hundreds of thousands to millions annually.

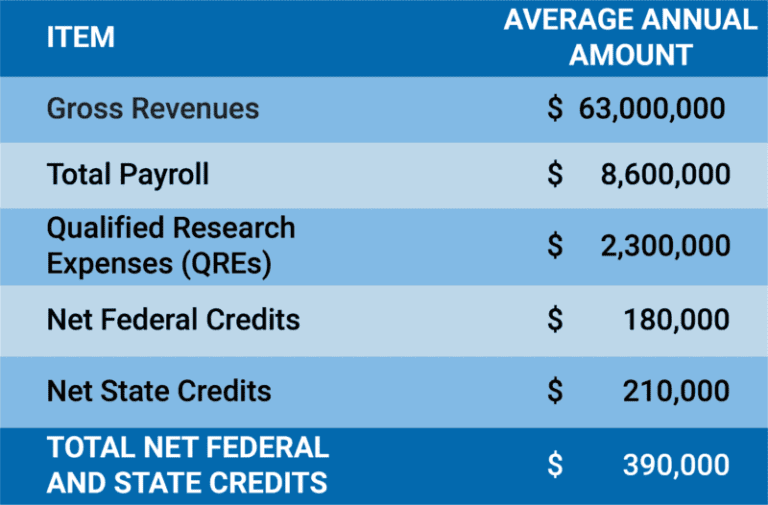

Food Manufacturers CASE STUDY