Manufacturing Companies

The R&D Tax Credit Explained

The Research & Development (R&D) Tax Credit is a federal incentive that rewards manufacturers for innovation, efficiency improvements, and problem-solving in the production process. Despite the name, “R&D” doesn’t just mean lab coats and scientists — it includes everyday engineering, prototyping, and process enhancements in manufacturing operations.

If your manufacturing company develops or improves products, processes, techniques, or systems, you likely qualify.

QUALIFYING ACTIVITIES

- Designing or improving manufacturing processes

- Developing prototypes or samples

- Reducing scrap or waste through experimentation

- Improving energy efficiency in production lines

- Developing custom tooling, dies, or fixtures

- Testing alternative materials or components

- Automating manual processes using robotics or software

- Engineering compliance with environmental or safety regulations

WHAT cAN BE CLAIMED

Manufacturers can claim:

- Wages for employees involved in design, testing, process engineering, QA, or tooling

- Supplies used in prototypes or test batches (not for sale)

- Contract research (e.g., third-party engineering or testing services)

- Software development (e.g., custom ERP or automation controls)

- Cloud computing expenses related to software development or modeling

WHAT DOESN'T QUALIFY

Certain activities are explicitly excluded:

- Routine QA or inspection (unless tied to experimentation)

- Reverse engineering (without improvements)

- Duplication of existing products

- Market research or consumer testing

- Foreign R&D (outside the U.S.)

- Capital expenditures (e.g., buildings or machines)

HOW THE CREDIt WORKS

The R&D tax credit is a dollar-for-dollar reduction in your federal (and possibly state) tax liability.

If you’re a startup or have minimal income tax liability, you may apply the credit against payroll taxes (up to $500,000 per year).

Unused credits can typically be carried forward for 20 years and backward 1 year.

Average R&D Tax Credit for Manufacturers

Credits vary by size and activity level:

Company Size | Average R&D Credit |

Small manufacturer (1–25 staff) | $25,000–$100,000/year |

Mid-size manufacturer (25–100) | $100,000–$500,000/year |

Large or multi-site operations | $500,000–$2M+/year |

These numbers increase significantly with systematic tracking and proper categorization of qualifying costs.

For Small to Mid-Sized Manufacturers

Even without a formal R&D department, small firms qualify for:

- Testing and tweaking production processes

- Custom fabrication or tooling

- Supplier material trials

- Prototype development and iteration

- Automation enhancements using off-the-shelf or custom software

Often, they underclaim because these activities are seen as “just part of the job.”

For Larger Manufacturers or Multi-Location Operations

Opportunities expand to:

- Dedicated R&D engineering teams or labs

- National-level process standardization and optimization

- In-house automation or robotics development

- Advanced material science research

- Software and system integration

- Environmental innovation or energy-saving initiatives

Proper time tracking, project documentation, and financial systems unlock high-value credits.

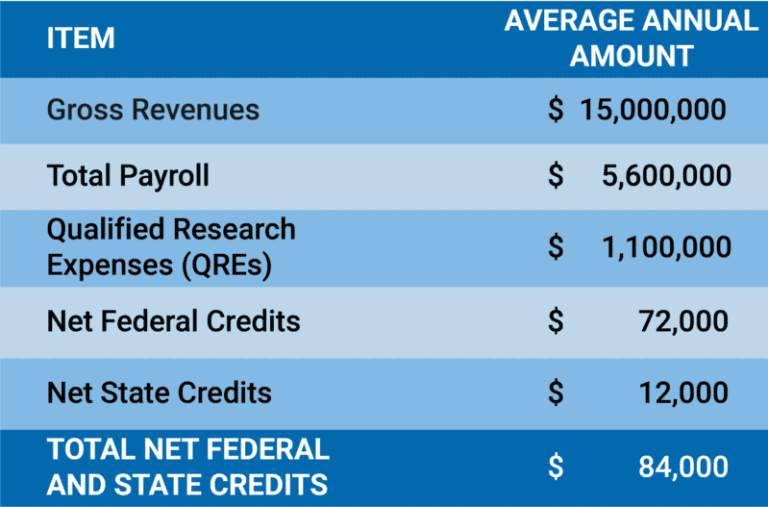

MANUFACTURING CASE STUDY