Architecture Companies

The R&D Tax Credit Explained

The R&D Tax Credit is a federal (and often state) incentive designed to reward companies that invest in innovation, technical problem-solving, and the development or improvement of products and processes. Architecture firms often qualify because they routinely design new structures, develop innovative building systems, use new materials, and integrate sustainable or energy-efficient solutions.

Even though “R&D” often evokes labs or scientists, architectural innovation—especially when solving technical design problems—qualifies under IRS guidelines.

QUALIFYING ACTIVITIES

Architecture firms can qualify for the credit by engaging in activities that meet the IRS’s four-part test: technical uncertainty, process of experimentation, reliance on hard sciences, and a permitted purpose (improving function, performance, reliability, or quality). Common qualifying activities include:

- Designing custom, energy-efficient buildings

- Developing sustainable or LEED-certified structures

- Experimenting with new materials or construction techniques

- Evaluating alternative structural systems

- Modeling daylighting or airflow to optimize building performance

- Integrating new energy or HVAC systems with innovative designs

- Using BIM or other modeling to resolve design conflicts

- Testing load-bearing alternatives or seismic reinforcements

WHAT cAN BE CLAIMED

Architecture firms can claim the following Qualified Research Expenses (QREs):

- Wages: Salaries of architects, engineers, and technical staff involved in design, modeling, or solving building design challenges

- Supplies: Costs for physical models, mock-ups, and prototype materials

- Contract Research: Third-party consultants, engineers, or energy modelers engaged in technical tasks

Cloud Computing: Costs associated with software used for experimentation and technical modeling

WHAT DOESN'T QUALIFY

Some activities and expenses fall outside the scope of the R&D tax credit. These include:

- Aesthetic-only design (without technical innovation)

- Standard designs reused without modification

- Routine drafting or documentation work

- Feasibility studies or planning with no experimentation

- Work performed outside the U.S.

- Sales, marketing, and admin tasks

HOW THE CREDIt WORKS

The R&D tax credit is a dollar-for-dollar reduction in federal income taxes owed. It can also be applied toward payroll taxes (up to $500,000/year) for qualifying small businesses and startups.

- You do not need to be profitable to claim

- You can carryforward unused credits up to 20 years

- States like CA, NY, and TX may offer additional credits

Average R&D Tax Credit for Architecture Firms

Your actual credit depends on the scope of projects, staffing, and how well technical work is documented. On average:

Firm Size | Estimated Annual Credit |

Small firms (under 25 employees) | $20,000 – $100,000 |

Mid-sized firms (25–100 employees) | $100,000 – $500,000 |

Large or multi-office firms | $500,000 – $2 million+ |

Firms working on LEED, WELL, or Passive House projects often qualify for larger credits due to increased experimentation.

For Small to Mid-Sized Architecture Firms

If your firm works on unique commercial buildings, custom homes, or sustainable projects, you likely qualify—especially if you:

- Use BIM for clash detection or energy modeling

- Solve design issues involving site constraints

- Incorporate passive solar or daylighting analysis

- Customize HVAC or structural layouts for unique sites

Even firms without a dedicated “R&D department” can qualify—what matters is the technical design work done on a project-by-project basis.

For Larger Architecture Firms or Multi-Location Practices

put content here for this section

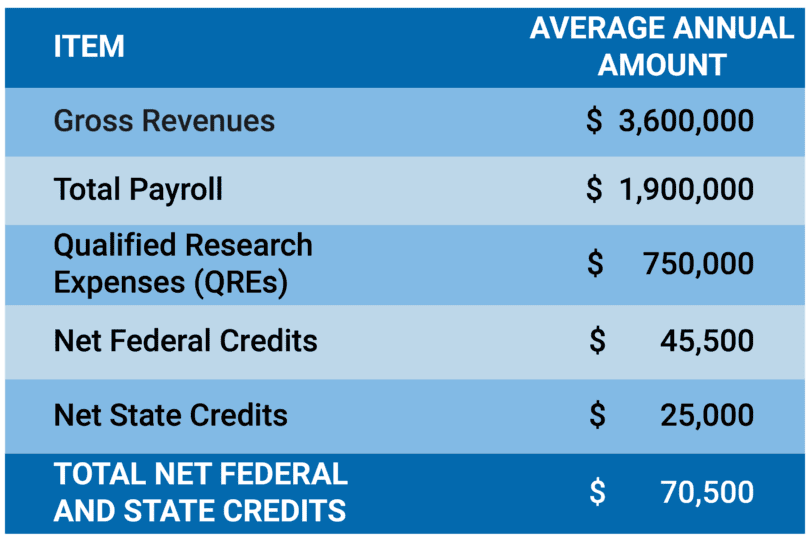

ARCHITECTURE CASE STUDY