Beverage Manufacturers

The R&D Tax Credit Explained

The R&D (Research and Development) Tax Credit is a federal (and often state) incentive that rewards companies for developing or improving products, processes, or technologies. For beverage manufacturers, this includes everything from creating new drink formulations to enhancing production efficiency.

You do not need a formal lab or wear lab coats to qualify—if you’re solving technical challenges related to beverage production, you may be eligible.

QUALIFYING ACTIVITIES

To qualify, the work must meet the IRS’s four-part test: be technical in nature, aim for improvement, involve uncertainty, and follow a process of experimentation.

Common qualifying R&D activities include:

- Developing new drink formulas (e.g., low sugar, plant-based, functional beverages)

- Reformulating existing beverages for shelf-life or taste improvements

- Experimenting with preservatives, carbonation, or natural sweeteners

- Designing new bottling or canning processes to improve speed or reduce spoilage

- Testing packaging innovations (e.g., recyclable, biodegradable, temperature-resistant)

- Implementing automation or robotics in the production line

Creating custom software for inventory, quality control, or traceability

WHAT cAN BE CLAIMED

Beverage companies can claim expenses known as Qualified Research Expenses (QREs) such as:

- Wages for employees involved in R&D (food scientists, process engineers, quality assurance)

- Supplies used in testing and prototyping (e.g., ingredients, bottles, labels)

- Contract research with third-party labs, food technologists, or flavor consultants

- Software development related to formulation, tracking, or quality improvements

WHAT DOESN'T QUALIFY

Not all work counts. The following do not qualify:

- Routine quality control or batch testing

- Marketing research or consumer surveys

- Cosmetic changes without technical uncertainty

- R&D conducted outside the U.S.

- Work after commercialization (e.g., scaling up production with no changes)

- Acquiring pre-existing formulations or recipes

HOW THE CREDIt WORKS

The R&D tax credit reduces your federal income tax liability. Startups may also apply it against payroll taxes (up to $500,000/year).

Key features:

- Both state and federal credits may apply

- Can be carried forward for up to 20 years

- No need to have a formal R&D department

Must retain documentation (payroll, project notes, test results)

Average R&D Tax Credit for Beverage Manufacturers

The amount varies widely by company size, R&D intensity, and recordkeeping quality. Estimates:

Company Type | Estimated Credit Amount |

Small Beverage Brands | $10,000 – $75,000 annually |

Mid-Sized Manufacturers | $75,000 – $300,000 annually |

Large Multi-Product Companies | $300,000 – $1M+ annually |

For Small to Mid-Sized Beverage Manufacturers

These companies often qualify by:

- Experimenting with small-batch flavors or functional ingredients

- Reformulating for calorie/sugar reduction

- Adapting production methods for limited-edition or seasonal beverages

- Creating more sustainable packaging options

Even if the company lacks formal documentation, strong internal notes and payroll records can support a valid claim.

For Larger Beverage Manufacturers or Multi-Location Operations

Larger beverage companies benefit from:

- Dedicated product development or food science teams

- Robust internal documentation of trials, QA, and pilot batches

- Investment in automation, robotics, or software for production

- Multiple concurrent R&D projects across locations or brands

These companies often qualify for six-figure or even seven-figure credits when properly documented.

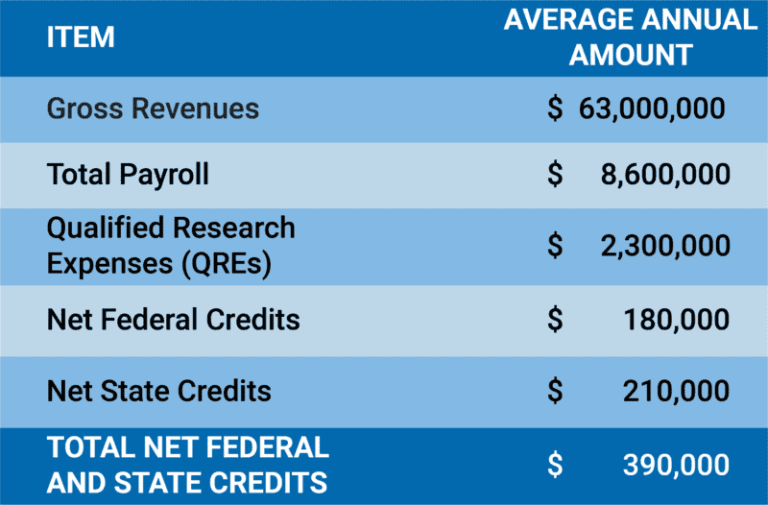

Beverage CASE STUDY